FURNITURE RETAILERS AND DECLINING ONTARIO HOME SALES

By: Paul J. Franchi LL.B, MBA, CIRP, LIT Baigel Corp.

My November 2022 presentation on Insolvency in Scarborough, Ontario connected me with hundreds of local professionals engaged in the Furniture Distribution industry and dozens of furniture retailers. Within months, I found myself knee-deep in my first furniture retailer bankruptcy and receivership. This experience revealed insights that extended beyond the furniture sector, offering a unique lens from the perspective of the unfolding dynamics of the Greater Toronto Area’s real estate sales slowdown.

RETHINKING REAL ESTATE METRICS

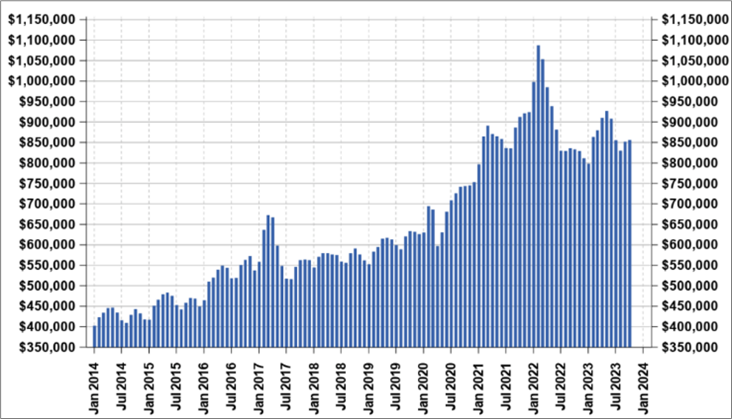

While many gauge the strength of the real estate sector through the lens of house prices, a more profound indicator lies in home sales volume. The trend in home prices in Ontario over several years demonstrates a stable and steady rise over time (see chart below). Many analysts will conclude this to be a positive trend when considering the impact this may be having on industries that are related to the real estate sector such as furniture sales.

Exhibit 1: Residential Average Price (Ontario)

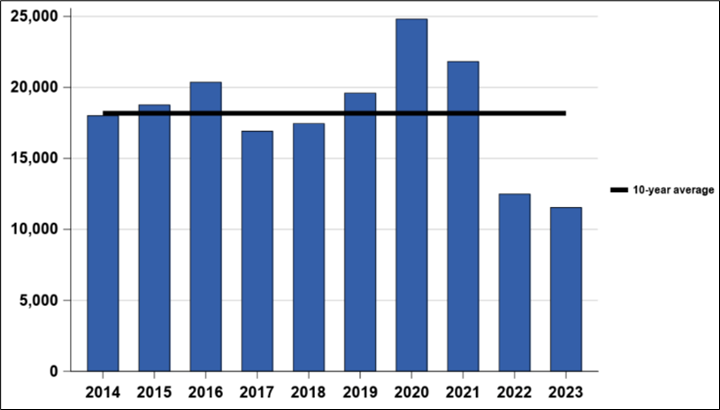

The more important metric is not the prices of homes but home sales volume also referred to as “activity”. In marked contrast to home sales prices, activity has plummeted by 50% from the high to well below the 10-year average (see Chart below). This is unleashing a ripple effect that directly impacts many people, from the furniture suppliers to real estate professionals, mortgage lenders to real estate lawyers. Statistics supporting this follow below. While the impact travels up the chain to furniture manufacturers, their shippers and retail landlords, this article particularly references the retail furniture space.

Exhibit 2: Residential Sales Activity (October only, Ontario)

It follows directly that if there is 50% less residential sales volume, then every business connected to that volume will be impacted. For example, fewer house moves, less home inspections, less real estate agent activity, less financings, less drone photography orders, etc. You get the message. Collectively they had half the sales.

Looking at the 2017 through 2021 growth in volume many businesses (such as the New Entrants segment as discussed below) invested borrowed funds (at the then low cost of capital) to expand their capacity, floor space and inventory to take advantage of the growth in activity volume they were experiencing. When the growth turned 180 degrees they had the double whammy – less sales and greater overhead.

Bad Boy Furniture Warehouse Limited (Bad Boy)

From the First Report of the Proposal Trustee In The Matter of Bad Boy Furniture Warehouse Limited (Bad Boy), we learn that the Trustee was initially engaged to provide non-restructuring services in March 2021. After that it had no further material role with the Company until March 2023.

During the two years that Bad Boy was not engaged with the Trustee, I was canvassing the street and obtained a firsthand look at what was unfolding in this industry. When Bad Boy’s unfortunate news hit, I was not surprised. Big and successful as they had been for an extended time, they were never going to be immune to the (mis)fortunes of the sector. Folk simply do not buy as much new furniture for the existing home as they may for a newly purchased home.

Canvassing the Industry

In my discussions with Furniture sector principals in November 2022 – often by simply making the rounds of retail locations, I noticed a definite absence of store traffic and groups of salespeople huddled or just “hanging out” at different times on weekdays and weekends. When I would inquire about the state of demand in the industry, many claimed that this was the “slow season.” One of my key contacts at the time was an owner who supplied my own home with some furnishings. At his Kennedy Street location, he told me candidly at that time, “Things are slow. Whoever tells you furniture is not slow is not being truthful. We’ve been through these cycles before, and we are financially and mentally prepared for this. We’ll see if this is a trend… hopefully not.”

When the central bank pulled the levers to reign in consumer demand (higher interest rates), it had the simultaneous impact of increasing the cost to suppliers of goods and services with leveraged business models. Less demand for, more expensive goods. The zombie companies that had relied on cheap capital are facing the new reality.

From these exchanges, I discerned that there were distinct segments in this marketplace. What is clear is these market segments were unevenly prepared for a sustained lower sales volume and may not make uniform usage of the full array of insolvency remedies available in future.

SEGMENT 1: Large Corporates

Dominant players in this segment are Leons, Ikea, Bad Boy, The Brick, Structube Canada, and others. These companies, due to their size, can entertain sophisticated restructuring proceedings when cost cutting, working capital reductions, landlord and supplier negotiations, etc. fail to produce the needed results.

At the time of filing, Bad Boy was a 12 retail store chain plus an e-commerce platform with 275 employees, and $16.1m in inventory and accounts receivable. Laurentian Bank served as the Company’s operating line of $4,000,000. According to the various filings by the Proposal Trustee, when Laurentian Bank issued its s.244(1) notice of default and demand and a Notice of Intention to Enforce Security, Bad Boy slowed this freight train down by filing a Notice of Intention to Make a Proposal (“NOI”) pursuant to the Bankruptcy and Insolvency Act (the “BIA”). Often what we see with companies of this size and complexity is a CCAA filing. This is not to say that a CCAA filing will not potentially follow instead of a proposal pursuant to the BIA. Despite proceedings commenced by way of the BIA, the motion returnable before the Honourable Mr. Justice Penny, sought (and obtained) relief that in Bad Boy’s counsel’s own words, “is consistent with the provisions customarily granted in proceedings under the Companies’ Creditors Arrangement Act.” Bad Boy obtained an Order prohibiting vendors from discontinuing or terminating contracts, leases, or other agreements with the Company, and to prohibit vendors from effectuating “pre-post set off” in order to withhold post-filing amounts payable to the Company on account of pre-filing obligations owing. Bad Boy has $15,392,000 in Accounts Payable owing and $4,544,000 in customer deposits which represent unsecured claims (since these funds were not held in trust). It sought this relief to “allow the Company to operate without disruption during the NOI Proceedings” and it was also stated that … “In order for the Company to deliver appliances to certain real estate development clients of the Builder Business … the Company requires the ability to purchase inventory and therefore the Company [was] requesting that the Court issue an order requiring vendors to continue to supply to the Company.” Bad Boy sought and obtained an Order for a liquidation sale to allow it to close inefficient parts of the business and to facilitate a restructuring. While smaller corporations may not be able to access all the solutions (including some tailor-made restructuring steps) they can still access formal relief and restructure successfully.

SEGMENT 2: Small/Mid-Sized Professionally Run Businesses with Decades of Experience

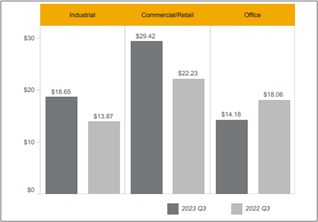

Looking at the GTA’s Kennedy Road strip we find seasoned smaller operators with fewer than four showrooms but with strong street-level visibility. This translates across Canada. The bankruptcy and receivership I managed in March 2023 (“Retailer”) falls into this segment. Clearly, there was a disconnect between what many sector owners were telling me in the November 2022 through April 2023 period and what the principals of Retailer were showing me. It was made clear to me that sales as early as then had approximately halved in contrast with business costs (including inventory, payroll and commercial/retail rent which had skyrocketed. The TRREB Commercial Network Members graph below shows a 32% increase in the rent that the furniture stores would expect to pay when comparing Q3 2022 to Q3 2023.

Exhibit 3: TRREB MLS® System Average Lease Rates ($/Sq. Ft. Net)

These businesses have founders who draw upon decades of hands-on and sometimes generations of experience and who vividly recall economic/real estate downturns like the 1991 meltdown. That is no guarantee they will survive this round. Perhaps by commencing proceedings by Division One of the BIA, Bad Boy may have set a trend for smaller players who have the need to access a lower cost and more efficient process than the CCAA route yet, where necessary, accessing certain creative restructuring solutions that are often found in CCAA proceedings.

I explored the realities of this segment with an industry veteran who had been involved in the furniture business since the 1980. He offered sagely advice: “The issue for this industry is not home prices. If anything, if home prices are too high, the impact is it leaves less money over for the home buyer to spend on furniture and appliances. What hurts us most is when home sales volume is down.” There is a direct correlation between sales volume in the residential housing sector and the market for furniture, appliances, and décor.

Whereas Bad Boy can boast over $10,000,000 in inventory, the players in this segment are usually less than one-tenth that at cost. Liquidation value can often exceed cost in a retail environment but that requires all the costs associated with running a sale.

With inventory likely being the most valuable physical asset for a Receiver or a Trustee to address an insolvency professional will need to consider several potential solutions such as a bulk sale, retail liquidation (including location of same), on-line auction, ongoing operations under the protection provided by a proposal, etc.

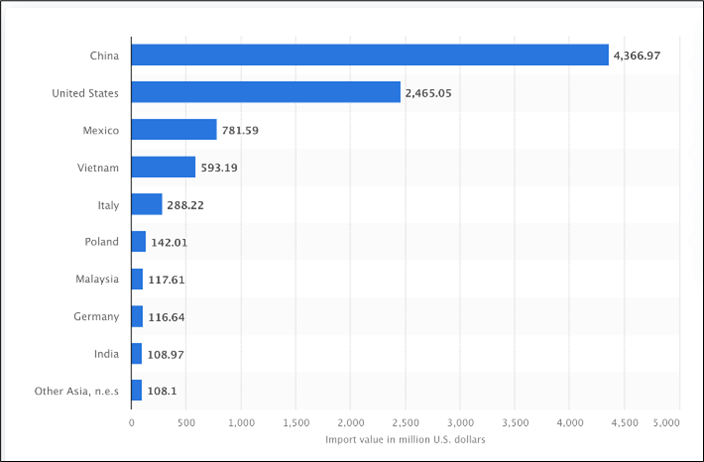

In this segment, an additional challenge the insolvency professional will face is that the business may well have its “custom” own method of tracking inventory – as rudimentary as an Excel spreadsheet. Their warehouses bear no resemblance to the orderly displays of their showrooms. Physically opening boxes to count all the inventory may be impossible or cost prohibitive. Most lower-cost furniture is sourced from China which may (and in my case did in fact) increase the burden of the task of taking inventory because of language and labeling challenges. (See chart below). If cartons must be opened to determine their contents, and if items come in sets as opposed to being sold as single units, then the cost of storage, security, labour, inventory management, assembly, and transportation can quickly become uneconomical in a Trustee’s task of realizing value when the cost of the inventory is below $1,000,000.

Exhibit 4: Value of Furniture Imported to Canada in 2021, by country of origin

I discussed these challenges with a reputable liquidator in the Retailer bankruptcy, who opined that a warehouse full of boxed furniture that was to be assembled has a negative valuation and that he would not remove it for a Trustee even if the goods were free of charge.

SEGMENT 3: “multi” Family-Owned Conglomerates

Interviewing leaders of long-standing family-owned businesses, I noted a resilient segment with significant years of experience in the industry which is “multi” family owned. The conglomerate arises when one or more families (usually within a distinct ethnic or faith group) combine resources to operate multiple businesses. Diversification exists across two dimensions: 1. Number of families sharing risk, and 2. Number of different businesses. These conglomerates are able to support a business facing challenges with resources from the other businesses. They take a longer-term view.

Many conglomerates leverage marketing to their specific ethnic community as a primary strategy (language, location, style, referrals, and affordable marketing reach advantages). In most cases, these operations were one large showroom, no warehouse and the furniture was shipped directly into the showroom. One business owner in this segment confidently asserted in April 2023 “Our family business has no debt. All the furniture you see in our store is fully paid for. We will never need insolvency services because we can wait out this slow period no matter how long. Our other businesses today are not slow at all.” The key to success it was indicated to me was to involve several families with multiple revenue streams across a few unrelated industries. These families demonstrated the strong immigrant ethos and all in the family/ies pull together using income from their multiple businesses, employment and sharing the strain of retail shifts. Unfortunately, long enough hard times bring many a previously sound partnership to a bitter end.

SEGMENT 4: Recent Entrants

A distinct segment comprises Recent Entrants whose business formation occurred in the past five years. Recent Entrants demonstrate marked differences in experience, with some lacking substantial industry knowledge and/or familiarity with local laws.

Many Recent Entrants were quick to leverage government stimulus benefits and financing. As a result, Recent Entrants now find themselves “all in” relying on personal credit cards and familial support to keep operations afloat. This segment is the most exposed because they have business models which in 2020 and 2021 showed promise because of rapid growth (as noted above) and are now grappling with higher fixed costs, reduced demand, higher interest rates and increased cost of maintaining an attractive inventory level.

I have sadly concluded that the Recent Entrants often have limited options at the corporate insolvency level. Usually, all the corporate assets are fully pledged and there are deemed trust claim assertions that rank ahead of the secured creditors. The loan sizes are generally below the level required to garner the attention of the secured creditor’s in-house professionals to effect the more sophisticated restructuring strategies.

What compounds these problems is that the owners’ personal affairs are tightly interwoven with the fabric of the corporate business – personal guarantees included. It is not unsurprising to me to see one owner change locations multiple times while changing the name of the company (or operating name), the legal entity conducting operations, and the partners or business associates who are involved or exercise equity ownership over the franchise in its various iterations. Determining which business names and individuals to conduct a PPSA search on can be surprisingly complex. Then matching the assets to these numerous entities PPSA searches adds another layer of work when the owner bought some of the furniture inventory two corporations ago, other in her personal name and has since combined it in a showroom with a new partner’s inventory. My view is that businesses in this segment may attempt to informally liquidate operations over time with their own “clear out” sales and one day simply “turn off the lights”.

Negotiations are taking place all over the map these days, with landlord arrears (distraint risks), secured creditors issuing demands and unpaid suppliers wanting to take back inventory. All this occurring under the overarching (if surprisingly quiet) issues of deemed trust rights of the CRA. Depending on the value of the remaining inventory and equipment these Landlords and Secured Creditors would likely benefit from a Licensed Insolvency Trustee’s perspective especially once they consider the Deemed Trust remedies available to the CRA as well as WEPPA obligations they may be inadvertently assuming.

While there may be little appetite for a principal from this segment of the industry to undertake sophisticated restructuring maneuvers for their corporation at the level of the Bad Boy proceedings, there is opportunity for the principals to, at a minimum, deal with their personal liability issues. This is because the store owner will continue to remain personally liable for liabilities and responsibilities which include unpaid wages and vacation pay, unremitted GST, personally guarantees etc.

Update from My Trusted Contact on the Street

I asked my close Furniture contact on the street for an update for this article, and his musings are:

“The economy sucks. In the past few months, it has got worse not better. We have been in a recession for over one year from where I stand and there are no signs of things getting better. There are implications for other industries. People are pulling back on what they absolutely do not need. Along with housing, their family, and their car, the priority is basic groceries and everything else is suffering.”

Conclusion

As the furniture industry grapples with increased operating costs during a time of reduced sales, the different segments are all facing challenges. They need the right advice and the right solution for their specific situation. The industry, like a shifting chessboard, requires astute moves and adaptability, with each stakeholder holding a unique piece of the puzzle. If one follows the old adage, the sooner a stakeholder reviews their situation with an LIT, the more options they are likely to have.

Please contact Paul if you would like to discuss this research.

Paul Franchi LL.B, MBA, CIRP, LIT

Baigel Corp., Licensed Insolvency Trustee

Direct: 647-484-5225

franchi@baigel.ca

The author acknowledges the input and contribution of Jeremy Kroll, CPA, CA, CIRP, LIT Baigel Corp