Market Segment Review

A Condo Purchaser’s Nightmare: When Is a Proposal to Creditors a Possible Solution?

By: Paul J. Franchi LL.B, MBA, CIRP, LIT and Jeremy Kroll, CPA, CA CIRP, LIT, Baigel Corp.

What, at the time of the commitment, seemed like a no-lose investment or home purchase, with a sale agreement signed (hereinafter “APS” or “APS Agreement”) and deposit placed on a condo, townhome, semi, or fully detached home, is today causing overwhelming stress for many who now find themselves unable to close their real estate transaction. Many people simply cannot obtain or afford the financing at current rates. They face the reality of being sued. This article suggests another potential solution to be explored.

This article is written as an aide to professionals who advise client purchasers of preconstruction real estate (Pre-Con), where the transaction has not yet closed and where there is concern that the purchaser has “bitten off more than he or she can chew.” While it has general applicability to any purchase and APS Agreement, the focus is on properties that were purchased months or years in advance of the expected completion date.

Pre-Con Purchasers Biting Off More Than They Can Chew

Purchasers who we speak to that are caught in this difficult position are often suffering from an unhealthy dose of denial regarding the inevitability of their fate. They reach out to professionals in search of a miracle remedy. Given that the APS was written by the developer for the developer there is no faint hope clause, no sympathy from the developer (themselves usually under stress) and the role of the professional is to guide the purchaser to the best possible outcome based on his or her situation. We have referred to both developers and builders as “vendor” throughout[i]. Until a Statement of Claim is issued and served upon the purchaser by the vendor, many purchasers are frozen in indecision and are unwilling to contemplate a proactive measure. The option of a formal proposal under the Bankruptcy and Insolvency Act (the “BIA”) can enable the purchaser to exercise a level of control over the timing and outcome of his or her situation and may provide leverage that otherwise would not exist to assist in negotiating an acceptable outcome as soon as possible. (The two types of proposals in the BIA are hereinafter referenced as “Consumer Proposal” and “Division I Proposal”, or “Proposal” when referencing generically).

BACKGROUND

The APS in a Pre-Con typically requires that the purchaser make a series of payments, typically 10-15% of the purchase price over a period of several months, and to be ready, willing, and able to close the balance of the transaction on the closing date which the developer specifies.

The “Genius Era” 2010-2022

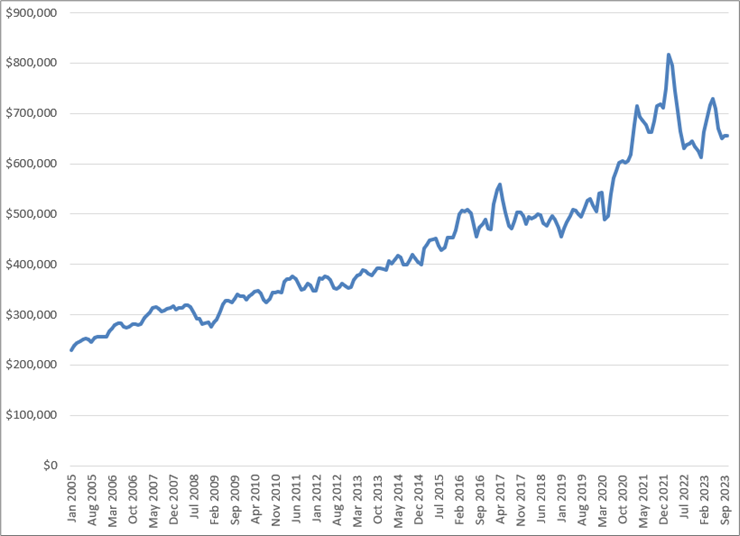

Pre-Con is not always a dirty word. It was not atypical for enterprising risk-takers to successfully make multiple bets on several Pre-Con developments with the intention of selling for a higher price even before their deal closed (a “flip”) and pocketing six-figure gains on each. This is because the trend in prices moved in the speculator’s favour for an extended period of time. Canadian housing showed a steady and predictable increase from 2005 to 2020 with a sudden hockey stick surge to 2022. This may have been responsible for attracting many speculators towards the end of the hockey stick. However, many Pre-Con purchasers who contracted in the 2020 through 2022 timeframe, with the expectation of a continuation of the trend, are sadly disappointed today because of both the pullback in prices from the peak and the significant spike in interest rates. Development is well behind the original estimated closing date in the case of many projects today and purchasers who are not able to close welcome such delay, perhaps feeling the relief that accompanies a stay of execution. Nonetheless it adds to the uncertainty – even if the delay enhanced the purchaser’s faint hope that time would deliver a solution.

Exhibit 1: Canadian Home Prices All Types

Source: CREA MLS HPI Aggregate Average Home Price Index

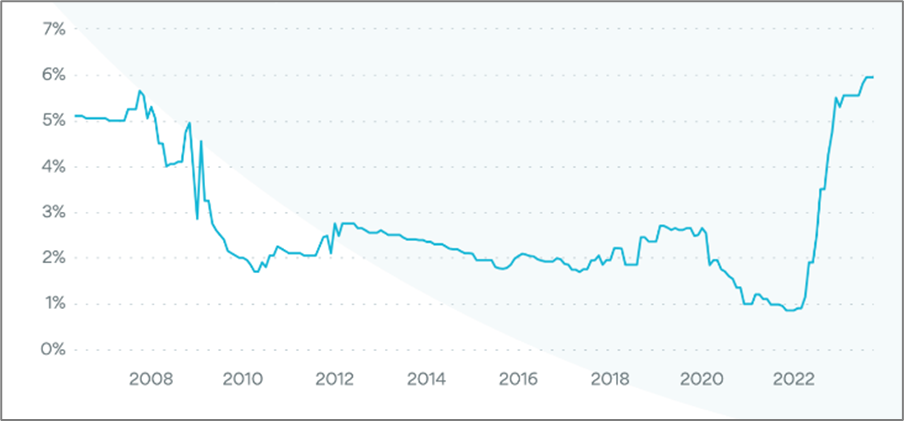

Very Cheap Money Went Away

Purchasers who were anticipating a continuation of the long-term established trend in declining interest rates were caught off guard by the increase in rates. While the most recent data, notably from the month of December 2023 shows a slight pullback or softening of the spike in variable and fixed rate loans, the current rates are still meaningfully higher than just one year ago.

Exhibit 2: Historical Discounted 5-year Variable Rates

Source: Rate Hub

EXAMPLE: Pre-Cons Not Meeting Appraisals – Buyers Not Getting Approval

The following example shows how these two trends are working against the purchaser. A purchaser obtained a pre-approval letter for a loan from a bank lender to purchase a $750,000 condo purchase on terms illustrated in the chart below. The purchaser would expect that with legal costs and land transfer taxes he would need to provide approximately $85,000 to close the transaction. The purchaser is expecting to make mortgage payments of $2,441.35 per month based on the 2.74%[ii]rate quoted in January 2022.

| Initial Deal Terms | Mortgage Details |

| $750,000 purchase price $10,000 closing costs $760,000 funds needed $600,000 first mortgage $75,000 deposit paid by installments $85,000 on closing | Lender Commitment Date: Jan 1, 2022 Term: 5-year fixed, 30-year amortization Rate: 2.74% Amount: $600,000 Monthly payment: $2,441.35 |

Fast Forward to the Present: January 12, 2024

The condo closing is now scheduled for February 20, 2024. The 5-year fixed rate, which was originally quoted at 2.74%, has now increased to 5.79%[iii]. The purchaser is waiting until the last possible moment to lock in a rate, hoping for more favorable rates. However, the appraisal for the property comes in at $675,000, far short of the $750,000 purchase price, creating a significant deficit. The bank is willing, based on the terms of the pre-approval letter, to advance 80% of the appraised value or $540,000. The purchaser will now be required to make up the $60,000 shortfall with an independent source of financing. In our theoretical example, the purchaser would need to utilize a second or private mortgage at 19% effective rate[iv]. In reality, this source of financing has been utterly locked down and unavailable to deals such as this one since the loan-to-value exceeds the threshold. Just three years ago, in a growing market, these deals were generally available. Illustrating the financing conundrum in the example, the purchaser’s monthly mortgage cost has spiked by 68%.

If the purchaser in our example is like many consumers, his or her wages have probably not kept pace with rising inflation in recent years causing an unsustainable reliance on credit cards and other forms of borrowing to cover living expenses each month.

Other Indicators This Problem May be Systemic

The example provided is for a 1st-time purchaser who had been properly pre-qualified for the mortgage (and they still got burned 2 years later but due to factors outside his or her control).

Unfortunately, not all purchasers were properly qualified according to the prevailing credit and mortgage industry standards at the time of the purchase. Bad actors in the Pre-Con industry were apparently treating the pre-approval as a game they could rig. Because the institution providing pre-approval letters is not formally bound (they re-assess at the time of the closing), their due diligence can be at a lower standard than that for an actual advance. Lower standards mean the gaps for the purchaser to obtain pre-approval by faking, lying, and misleading are wider open. The purchaser who relied on a faked pre-approval letter has an even deeper hole than in our example. He or she not only has the movement in rates and appraisal values running against him or her, the hole is deeper to the extent that he or she does not have the income or assets he or she pretended to have in order to pre-qualify. For actual advances, the mortgagees will ask for documentary support.

| Revised Deal Terms | Revised Mortgage Details |

| $750,000 purchase price (same) $10,000 closing costs (same) $760,000 funds needed (same) $540,000 first mortgage (new) $60,000 second (private) mortgage (new) $75,000 deposit paid by installments (same) $85,000 on closing (same) | First Mortgage Lender Commitment Date January 10, 2024 Term: 5-year fixed, 30-year amortization Rate: 5.79% (new) Amount: $540,000 (new) Mortgage Monthly payment: $3,141.48 Second Mortgage Private/ interest only due in one year Rate: 19% Amount: $60,000 Monthly payment: $1,140 Combined Mortgage Payment: $4,094.76 |

Some insiders in the mortgage industry are privately acknowledging that, akin to financial markets like the stock market, merchant banking services, and project finance, exuberance can skew participants’ perceptions in real estate. The prolonged period of prosperity spanning multiple decades has nurtured complacency within the risk management and compliance departments of several lenders.

Vendors, in this case the developer, need to secure purchasers and meet lenders’ quotas as per their construction loan agreement to continue obtaining advances under the development funding arrangements. To enable the vendor to meet its own financing approval targets, certain developers chose to loosen their approval criteria on the front end when assessing the quality of purchaser applications.

An industry veteran who remembers the 1991 real estate crisis vividly recalls privately:

“Builders have been increasing accepting not only approval that come from the Chartered Banks and have the ‘full work up’ but also those of independent mortgage brokers who are of varying experience and reputations. In many cases I am witnessing, the mortgage brokers were not running a credit report or performing a proper investigation into the purchaser’s finances that would properly determine that he or she was qualified for the loan. Some of these guys were basically ‘giving away the letters”.

Traditionally, the pre-approval letter would state the address of the property, unit number and terms of loan (a ‘real term sheet’) that was required for developers to include the unit as ‘sold to an approved purchaser’. Friends in the legal community are sharing with us that they have seen a rise in aggressive speculators who utilize one legitimate pre-approval to secure multiple Pre-Cons. This activity is likely fraudulent and may carry with it serious potential consequences in the course of a formal insolvency proceeding (including a victim of such conduct seeking an order for the debt to survive the BIA proceeding).

The prevalence of fraud or even the lesser “negligent misrepresentation” has not been possible to establish empirically, and our observations are based on anecdotal information. One of the co-authors, while working in the finance industry in New York City, experienced firsthand the US subprime crisis as it unfolded. What is memorable for him today was listening to very seasoned fixed-income investment analysts as early as 2006 who got it completely wrong for similar reasons that may apply in this instance. These analysts and portfolio managers were too quick to dismiss as being significant, the tremors that were being felt at that time in the fraud-laden subprime mortgage segment of the US mortgage and housing industry. The tossed around belief was that since this segment comprised less than 2% of the overall mortgage market it could hardly be a systemic risk to the financial system. This time around, we don’t want to find ourselves equally incorrect about what the outcome could potentially be. We shouldn’t be too quick to dismiss insider observations concerning the capriciousness of many pre-approval and actual mortgage approvals. If a shakeout in the individual purchaser’s situation is inevitable, there are reasons (which will be further elaborated upon) for why it is usually beneficial to be proactive in seeking the opinion of a Licensed Insolvency Trustee (“LIT”).

Assignment Sales

Many speculators contracted to purchase multiple Pre-Cons following their earlier successes in prior transactions. Many of these speculators will readily admit that they had no intention of closing on the purchase but intended to ‘flip’ the property to another buyer for a higher price through an assignment sale before closing. An assignment sale involves a purchaser who transfers his or her rights as a purchaser in an APS to a new purchaser. At the moment, the speculators are finding an empty pool of would-be buyers to flip these investments to – even at a discount.

In most cases, an assignment sale requires the vendor’s consent and there is often a fee for providing that consent. In these more challenging times, certain developers are waiving the fee to enhance the likelihood that the APS will close as scheduled. Closing without disclosing a new buyer would likely be in contravention of the original APS (a contract breach). Importantly, the vendor will maintain its full rights against the original purchaser under an assigned contract -including the vendor’s potential losses if the assignee fails to close.

Other instances exist where the developer will refuse to allow the assignment so that the unit can be sold to a new purchaser at a higher price.

A successful assignment as a solution likely only works where the purchaser’s inability to close is based primarily on the financing side of the equation and where the purchase price makes sense, at least to the extent that it can be subsidised by the purchaser’s forgone deposit.

Where Pre-Approval Mortgage Lender Now Says “No!”

SCENARIO 1: Current Market Value Well Above The Contract Price

In situations where the value of the Pre-Con has appreciated substantially from the date of the APS to the closing date, the marketplace almost always has a solution to offer. In one non-insolvency example, a purchaser approached us on a Sunday morning in regard to a close the following day. Her lender could not come through because she could not satisfy the loan to value ratio. She had made a $100,000 deposit on a $500,000 condo, which had a current market value of more than $650,000, and she was going to lose $100,000 in deposit and the opportunity to realize a potential future $150,000 in capital gains. We introduced her to a trusted private lender who had a lawyer on standby for these types of emergency situations. A year later, she has been refinanced with a conventional big bank lender, and the process to get her there was at a cost that she was comfortable with paying.

Whether it is a second mortgage, a private loan, or taking on a partner who has equity to inject into the closing arrangements, there is rarely a problem without a solution when dealing with Pre-Cons that have significantly increased in value.

SCENARIO 2: Current Market Value Below The Contract Price

As we have alluded to in the case study example provided above, solutions are less abundant when the value of the Pre-Con declines in value because the purchaser will be required to raise additional capital in order to close. If the purchaser lacks the financial means and cannot find a partner to inject capital, or cannot obtain a loan from friends or family, the deal will simply fail to close. This is of concern today because we are witnessing an increasing number of assignment sales posted showing the assignor is willing to accept a loss on the assignment.

Among the purchasers in this scenario we have observed some uncertainty on their part about the potential liability if they are unable to close the APS. One source of confusion arises from a misconception that certain laws governing mortgage recovery rights are applicable in their situation, which is simply not the case. Specifically, in certain provinces and U.S. states, e.g., many insured mortgage arrangements in Alberta and Saskatchewan, borrowers who struggle with mortgage payments have the option to limit their liability. In such instances, they can simply mail their house keys to the lender (known in the USA as “jingle mail”). The lender’s potential recovery is restricted to whatever recovery they can obtain from the sale of the property and claim against the insurance policy, without further claims against the mortgagor. Instead, the correct operative legal principle when it comes to damages for breach of contract which is virtually universal across common law jurisdictions, states that “an aggrieved contracting party is entitled to damages that will return that party to the position they would have been in had the breach not taken place.” In other words, the vendor can sell the property that the purchaser refused to close on and continue to pursue the purchaser for the full extent of the vendor’s damages at law, which takes us to the next and related area of confusion.

This second source of confusion arises from the mistaken belief that the vendor will be limited in damages to the deposit paid by the purchaser. When the purchaser walks away from the deal, the vendor can and will claim for any losses arising from additional costs of having to sell the Pre-Con a second time. Any loss the developer suffers from having to sell the same unit for a second time to a new purchaser, but at a lower price than the original APS with the original purchaser is fully recoverable. Following a favorable judgment for the Vendor, it is authorized to pursue the purchaser’s assets including the usual wage garnishment, freezing of bank accounts and, in certain Provinces like Ontario, RRSP assets (RRSPs contributed more than 12 months prior are exempt from seizure if the debtor seeks protection by way of a Proposal or bankruptcy).

Purchaser May Have A Claim Against The Developer: Return Of Deposit Or Other Legal Recourse

Recent case law confirms that the vendor/developer’s right to keep the deposit in a failed pre-con real estate deal as a legal “forfeiture” is not automatic or absolute. If the developer’s actual losses were less than the deposit, Courts have ordered the developer to pay the difference to the Pre-Con purchaser in situations where it was found to be unconscionable for the vendor to retain the forfeited amount.[v] This was recently confirmed by the Court In the Matter of the Bankruptcy of Pleterski and AP Private Equity Ltd., 2023 ONSC 5546. The vendor has a duty to mitigate its damages and, in doing so, it may fully recover all losses suffered and even experience a surplus (e.g. selling at a higher price than the original APS). In such cases, a Court may order some or all of the deposit to be returned. When acting as LIT for a purchaser who has lost a deposit, the LIT may list as an asset, a claim for recovery against the vendor for some or all of the lost deposit if the unique set of circumstances as set out by the Court in Pleterski apply.

In some cases, the developer will deliberately keep the purchaser in the dark as to whether the developer has mitigated its damages (or better). The developer may be rather pleased to have nothing more to do with the purchaser whose deposit it has kept. That said, we believe the developer will force a purchaser to extract that information from them via the legal process (which means the purchaser would need to pay legal fees). In a bankruptcy or Proposal scenario, if there is potential value for the estate, the LIT (or the creditors themselves pursuant to section 38 of the BIA where the LIT refuses or neglects to act) will bear the cost of obtaining the details from the developer. It is noteworthy, that where a developer fails to respond to a demand to file a proof of claim by the LIT, the developer may be signaling it has no claim to file and that the estate may have a recovery opportunity.

A purchaser may in certain circumstances, have an unrelated separate right of damages against the vendor. Whether this stretches to the purchaser having the right to refuse to close must be determined using what has become a stringent legal test in the Province of Ontario. The tests are summarized in Tse v. Sood (2015) OJ No 495. This case is cited because it is one such case where the purchaser was found to be entitled to a recission (voiding) of the APS and return of her deposit money. The occasions where there is no requirement to close fall under four broad categories and involve a vendor who has: 1. Failed to satisfy a condition precedent, 2. Committed a “fundamental breach”, 3. Failed to convey good title, or 4. Is found to have made a misrepresentation. It is usually the case during any real estate down cycle that the Court dockets quickly fill up with litigation involving armies of purchasers who have refused to close and whose lawyers are making often ham-fisted efforts to fit their case into one of these slots. One co-author notes this from his personal experience where he once practised as a litigation lawyer and acted on several of these types of cases. The occasions where a Court rules squarely in favor of the purchaser, as in Tse v. Sood are a very infrequent occurrence. However, it must be stated that if these factors may be present, the purchaser is always well advised to consult with a litigation lawyer well versed in real estate matters.

Purchasers, or their advisors, who are already financially distressed when faced with an upcoming Pre-Con closing that cannot close should consider obtaining an LIT’s perspective on the situation.

BIA Proposals – More Efficient, Effective, and Economical Than Waiting to Be Sued?

Background Information on the BIA For Non-Insolvency Practitioners

Protection under the BIA provides purchasers with rights when their debts exceed their ability to repay. Canadian law enables the honest debtor to make a Proposal to his or her creditors or to assign him or herself into bankruptcy. These are formal processes and must be made through an LIT. A Proposal can be as creative as the circumstances call for and can include the debt to the developer even if the precise amount owing is not conclusively established at the date of filing. It can be useful to select an LIT with a high degree of knowledge of the Pre-Con shortfall world. Developers will often be the largest creditor which generally means they may have the greatest voting power in the Proposal.

As mentioned the BIA provides two types of Proposals. For individuals whose debts do not exceed $250,000, excluding the mortgage on their principal residence, the Proposal is made pursuant to Division II (a Consumer Proposal). This is a more streamlined process (allowing for deemed creditor acceptance and deemed court approval, a simplified voting mechanism, a regulatorily prescribed fee which is usually paid out of the funds otherwise offered to the creditors and no automatic bankruptcy on rejection or withdrawal). For those who do not qualify for the Consumer Proposal, they may file a Proposal pursuant to Division I. This has a more involved process but remains quite accessible. The main draw backs include mandatory voting by creditors with a higher threshold for acceptance, an actual approval hearing by the Court, automatic bankruptcy if not accepted or approved and, in some cases, the posting of security for the Proposal payments. The Division I Proposal has certain benefits such as: a “Notice of Intention to Make a Proposal” can be filed very rapidly and trigger protection from the creditors allowing 30 days (extensions are available through Court application) to craft and file the Proposal. Proposals are accompanied by extensive documentation which lay out the full financial affairs of the insolvent individual, a report of the LIT which will typically provide an opinion that the offer that is being made is fair and reasonable to creditors and that it is more favourable to the creditors than a bankruptcy scenario. Usually, the Proposal offers greater certainty as to timing, costs, and quantum and importantly the Proposal is not considered as a bankruptcy and this will usually facilitate a shorter path for the debtor to rebuild their credit bureau score.

Proposals and the Pre-Con Purchaser With No Options

The writers have found that most purchasers who come to us when they cannot close on their Pre-Con will choose a Proposal rather than bankruptcy. These purchasers typically have an ongoing income stream to protect and have simply miscalculated on the closing requirements for the Pre-Con. Debtors often assume that bankruptcy is their only remaining option due to them having no way of knowing the extent of their liability if they breach their APS. Part of our role as an LIT is to fully evaluate all options available to debtors and to inform them accordingly.

The Proposal is a negotiated contract with creditors that is enforceable by the Courts. It helps avoid the costs of extensive and drawn-out litigation thereby often rendering the Proposal the more proactive, affordable, efficient, and effective alternative.

BIA Efficient and Rules Based

The stakeholders, including the purchaser, benefit from the organized rules-based structure of the BIA with its myriad of mechanisms, time limits, and extensive case law precedents driving the entire process. It is generally a business-like process and practicality is a hallmark.

One such mechanism is that a skilled LIT will work with the purchaser/debtor and his or her professionals to estimate the amount of damages that the vendor would suffer if the purchaser failed to close. The vendor’s responsibility to mitigate its damages means the vendor must, where applicable, prove to the Court that it has taken active steps to reduce the total losses suffered because of the purchaser’s breach of contract. The LIT does not automatically accept the vendor’s proof of claim and ought to be vigilant in identifying potential hidden recovery to which the insolvent estate may be entitled – such as a refund of the deposit. As mentioned, in limited circumstances where it may be appropriate, it is our practice to include both a liability and an asset in Proposal documents. While this may seem incongruous, where the debt to the developer is contingent and any amount recoverable from the deposit (and/or other damages caused by the developer) are not known at the time of the filing, listing both the liability and the asset keeps both potential scenarios visible to all. Further, where appropriate, listing the debt to the developer as contingent may allow for the filing of a Consumer Proposal instead of filing under Division I because the total debts listed may fall below the $250,000 threshold. In some instances, the Proposal format and the actions of the LIT can drive a negotiated settlement without the expense and delays of litigation. Last, but not least, the purchaser can have closure as to his or her exposure.

BIA When Utilized Skillfully Forces an Early Resolution on Quantum of Damages

A Proposal covers all liabilities of a debtor as of the date of filing the proposal, including potential liabilities for debts that have not yet been crystallized. Such debts may be considered as contingent or unliquidated debts. For example, creditors who are threatening to sue or are in the process of suing, and the defendant’s liability is in question and has not yet been determined in a Court of Law, could have their claims to be considered as contingent claims, and such claims can be specifically included in the proposal process as provable claims by Section 121(2) of the BIA. Similarly, unliquidated claims, being potential debts that may not be ascertained by simple arithmetic calculation and may not be crystallized for months or even years, can also be specifically included as provable claims in a Proposal. Left alone to deal with these uncertainties, a purchaser in a Pre-Con will face ongoing costs, stress, and an inability to move forward taking a toll on the debtor’s mental health as well as his or her pocketbook.

Pursuant to section 135 of the BIA, the LIT is empowered to place a value on or disallow contingent and unliquidated claims. The amount may be disputed by the creditor advancing the claim and there is a mechanism to have that dispute addressed by judicial review. Some LITs, or the courts on appeal from the trustee’s decision, may require the creditor to separately establish the quantum of damages in a separate trial. An important point being made here is that, with the correct guidance of an LIT, contingent and unliquidated debts may be proactively dealt with. We must be mindful of the caveat that a decision by a court officer (be it trustee, registrar, associate judge, or judge) on the valuation of a contingent or unliquidated claim is subject to appeal all the way up the chain if the aggrieved creditor wants to take it that far. So, even the best of intentions to expedite an otherwise lengthy process could still be drawn out.

One important advantage in commencing a formal insolvency proceeding is that the BIA is, in and of itself, an entire conflict resolution regime. The BIA together with its Rules has been crafted with the intention of bringing these commercial disputes to a speedier conclusion than is generally experienced in non-BIA civil litigation matters. For example, a Proposal debtor in a Consumer Proposal will know with certainty within 45 days whether his or her Proposal is accepted by creditors or requires further negotiating. Debtors generally experience relief the moment they get clarity on their total liability owing and in knowing how much their monthly payment to creditors will be over coming years. The timing of an answer from the creditors and the Court is typically longer in a Division I Proposal but it compares favourably to the mire of civil litigation.

CONCLUSION

Pre-Con purchasers concerned about not closing should seek the insight of an LIT to evaluate if a formal Proposal under the BIA is suitable to their circumstances. If the purchaser is insolvent (or would become so when failing to close), cannot find a source of funds to close their deal, or if the purchaser can secure financing but lacks the means to service their existing or upcoming debt load, a discussion with an LIT is indicated. Litigation is often the first path for many who are unable to close on the APS but often fails to provide the solution that a purchaser needs in an effective manner. Most LITs offer an initial consultation on a no-charge basis. Lawyers, mortgage professionals, real estate brokers and accountants whose clients are facing concerns about closing can also contact the LIT, on a no-name, confidential basis, to obtain a sense of the LIT’s perspective.

Please contact Paul if you would like to discuss this research.

Paul Franchi LL.B, MBA, CIRP, LIT

Baigel Corp., Licensed Insolvency Trustee

Direct: 647-484-5225

Jeremy Kroll, CPA, CA, CIRP, LIT

Baigel Corp., Licensed Insolvency Trustee

(416) 224-4350

kroll@baigel.ca

[i] The APS is between the purchaser and the owner of the lands. Developers typically create specific use incorporated companies which own the land and contract with the Purchaser for a given project. Developers in some cases sell the land to a builder after zoning is complete and hence dealings pertaining to the APS are then between the builder (or builder’s numbered company) and the purchaser. In many cases a developer will build the project on its own and in such cases the developer and not the builder is contracting with purchasers. For this reason the terms “builder” and “developer” often get used interchangeably.

[ii] 2.74% is conservative. Depending on the purchase date many purchasers received indicative rates that were lower

[iii] 5-year fixed rate 30-year amortization non-insured 80% mortgage rate quoted as of January 2, 2024 (may vary).

[iv] 13.99% 2nd Mortgage Loan, 3% lender fee, 2% broker fee total 19% Note: lender and broker fees are typically deducted at transaction date but are being applied here as part of the monthly payment for illustration purposes. Also some (first) mortgage agreements require approval of the first mortgagee for this type of financing.

[v] A full explanation of the law of forfeiture and deposits in Real Estate transactions is beyond the scope of this article. Some lawyers will disagree with the stark statement made here and will argue that deposits are not liquidated damages and the developer gets to keep a deposit regardless of the mitigation steps. The following provides a summation of the law on forfeiture https://landscapeontario.com/liquidated-damages-deposits-and-forfeiture-clauses and specifically Aylward v. Rebuild Response Group Inc., 2020 ONCA 62, 2020 “A true deposit is an ancient invention of the law designed to motivate contracting parties to carry through with their bargains. Consistent with its purpose, a deposit is generally forfeited by a buyer who repudiates the contract, and thus is not dependent [as is a liquidated damages clause] on proof of damages by the other party”.